A “free” portfolio review feels harmless, maybe even generous. An advisor scans your holdings, flags a few gaps, and you leave feeling wiser. Yet, according to industry surveys, about 73 percent of investors don’t know what they pay in fees, or assume they pay nothing at all.

That blind spot is costly. Tiny, percentage-based charges compound in reverse, quietly siphoning thousands from long-term returns. This guide shines a light on them. We’ll show you the visible costs first, then expose five hidden fee layers, complete with dollar examples and must-ask questions.

Ready to keep more of what you earn? Let’s start with the price tag you can see.

What a portfolio review usually costs up front

Before we dig into hidden fees, you need a clear view of the price tag you can see.

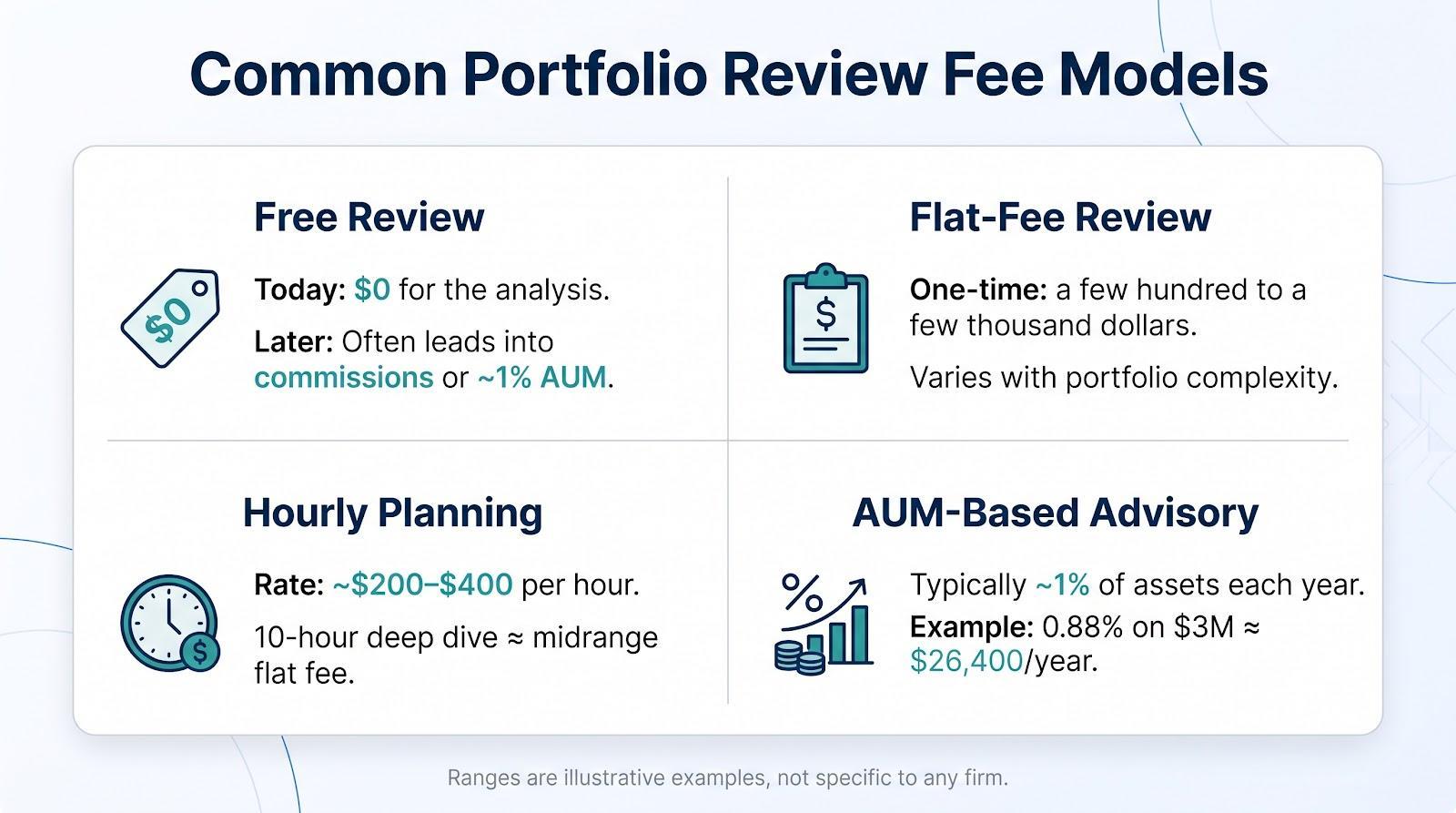

Most review services fall into four storefronts. Some advisors invite you with a “free” checkup. Others quote a one-time flat fee. A few bill by the hour for each planning session. The largest group folds the review into an ongoing assets-under-management (AUM) arrangement.

Sticker prices vary, yet patterns appear. A flat-fee diagnostic often costs a few hundred to a few thousand dollars, depending on complexity. Hourly planners run about two hundred to four hundred dollars per hour, so a ten-hour deep dive lands in the middle of that flat-fee range.

The AUM model looks friendly at first glance, just “about one percent” of assets each year. That small percentage grows fast. An industry study shows the average household with three million dollars pays roughly zero-point-eight-eight percent, or twenty-six-thousand-four-hundred dollars, every single year under this structure. Over a decade, that sum can rival the cost of a new home.

Free reviews cost nothing today but carry an unwritten expectation that you will move your money to the firm later. The real invoice surfaces in commissions or management fees.

Look for firms that spell out those numbers in plain English before you ever become a client.

As outlined on this portfolio analysis page, one nondiscretionary review model walks through four steps, a current-holdings assessment, a strategy evaluation, tailored recommendations, and ongoing monitoring, while you retain full control of every decision.

Disclosures like that give you a clear yardstick: if an advisor cannot match that level of transparency and duty, keep shopping.

Once you know these models, you can translate percentages into hard cash. That translation is step one in protecting your returns because every hidden layer we uncover next stacks on top of these headline numbers.

Hidden fee #1: the “free review” trap.

Nothing sparks our bargain reflex like the word “free.” Advisory firms know this and often offer complimentary portfolio checkups as an icebreaker.

The real goal is client acquisition. During the review, the advisor spots gaps and offers to fix them, so long as you transfer assets. Sign the paperwork and the meter starts. You move from a no-cost meeting to a one-percent AUM relationship or into commission-paying products.

Because the fee arrives later, it rarely feels linked to the original chat. That gap masks thousands of dollars a year. The advisor’s incentive also shifts; recommendations tilt toward products the firm sells, not necessarily the cheapest option for you.

Your defense is twofold. First, treat a free review as reconnaissance, not a contract. Take the findings home, think them over, and, if changes seem drastic, get a second opinion.

Second, demand transparency. Ask, “If I follow your advice, what will I pay next year in total dollars?” A trustworthy planner answers plainly and puts the number in writing. If the reply wanders into percentages, industry averages, or “don’t worry about it,” consider that the price of admission.

Hidden fee #2: fund expense ratios.

Even with a fee-only planner, money can still leak from inside the investments. The expense ratio is the annual cut a fund company takes to run a mutual fund or ETF.

Because the fee comes out daily, you never see a bill. Yet the drain is steady. An index fund might charge zero-point-zero-five percent, while an actively managed cousin sits closer to one percent. On a million-dollar position, that gap equals nine-thousand-five-hundred dollars each year.

Over time, the hit compounds. Vanguard’s Advisor’s Alpha study shows that swapping high-cost funds for low-cost alternatives can save about zero-point-three-four percent per year, or three-thousand-four-hundred dollars on a one-million-dollar account.

Expense ratios can also hide conflicts. Some share classes include a twelve-b-one trail that sends part of the fee to the selling broker. If your review suggests funds that cost more than similar index options, ask who benefits.

Your action item: request a list of every fund you own with its expense ratio and share class. Then calculate a weighted-average cost for the whole portfolio. If that number exceeds zero-point-three percent for a broad stock allocation, you are overpaying for market exposure.

Switching to lower-cost share classes rarely changes strategy; it just keeps more dollars compounding in your account instead of someone else’s pocket. That quiet upgrade can deliver the biggest return a portfolio review offers.

Hidden fee #3: commissions, loads, and kickbacks.

Some recommendations are less advice and more sales pitch. When a portfolio review ends with a suggestion to “upgrade” into a new mutual fund or insurance product, pause and ask who gets paid.

Many mutual funds still carry a front-end sales load of three to five percent. Invest one hundred thousand dollars and the fund can skim up to five thousand on day one, leaving you with ninety-five invested. A back-end load hides the bite until you sell, while a level load drips out each year. Different label, same wallet drain.

Next come twelve-b-one trails, which are ongoing marketing fees embedded in certain share classes. They can siphon up to one percent a year and send a slice back to the broker who sold the fund, keeping the revenue stream alive long after the paperwork is signed.

Insurance products cost even more. Variable annuities and cash-value life policies often pay the agent a five-to-seven-percent commission, baked into higher internal costs and steep surrender penalties. The complexity hides the charge, but you still face lower net returns and years of lock-in.

Spot these kickbacks in two ways. First, ask for the fund’s prospectus or the annuity’s fact sheet and look for words like “load,” “surrender,” or “twelve-b-one.” Second, ask the advisor, “Do you receive any commission or revenue share if I buy this?” A fiduciary advisor will answer no and steer you toward no-load, institutional-class funds.

When a recommendation is truly in your best interest, the numbers still work once commissions disappear. If the math collapses without those fees, the product was never meant to serve you.

Hidden fee #4: platform, account, and transaction charges.

Custodians and tech platforms keep your assets safe and your statements tidy, but they rarely work for free. Their fees arrive in small, easy-to-miss bites that add up fast if no one pays attention.

Start with the “program” or “wrap” charge. Some advisors outsource trading, billing, and reporting to turnkey platforms that add an extra tenth to half a percent each year. On a five-hundred-thousand-dollar nest egg, that surcharge alone can top two thousand dollars, money you may never spot because it hides inside one bundled line item.

Next come maintenance fees. Many brokers still bill sixty dollars a year for each IRA, plus “paper statement” or “inactivity” penalties when an account falls below activity targets. These charges feel minor in isolation, which is why they persist. When your portfolio sprawls across several small accounts, the drip turns into a steady leak.

Transaction costs have not vanished either. While stock and ETF trades now price at zero on most retail platforms, buying an out-of-network mutual fund can still trigger a forty-dollar ticket charge. Add a few specialty trades or bond purchases and the total rivals a modest advisory fee.

Even money in motion carries a toll. Transfer an old 401(k) and the departing custodian may ding each account seventy-five dollars. Wire funds for a property closing and the bank pockets another thirty.

You cannot eliminate every micro-fee, but you can spot and control them. Consolidate accounts when practical. Choose share classes that trade free. And ask your advisor one clarifying question: “Does your stated fee cover all platform, custodial, and trading costs, or will I see separate debits?” The answer will reveal whether these small charges stay small, or quietly grow.

Hidden fee #5: tax consequences and turnover costs.

Taxes never appear on an advisor invoice, yet they can become the largest cost when you overhaul a portfolio.

Picture a long-held fund with a forty-thousand-dollar unrealized gain in your taxable account. If a review suggests selling tomorrow, you may owe capital gains tax this April, roughly six thousand dollars for many investors, no matter how the new fund performs.

Turnover multiplies the hit. Advisors who trade often, or funds that churn holdings, create short-term gains taxed at ordinary income rates. Those rates can exceed thirty percent for high earners, far above the fifteen to twenty percent applied to long-term gains.

Even passive investors feel the pull when an actively managed mutual fund inside a brokerage account distributes gains each December. You never place a trade, yet you pay tax on someone else’s choices. Over time, these surprise distributions can shave one to two percent a year off net returns, a bite on par with an advisory fee.

Smart reviews weigh the benefit of moving today against the certainty of an immediate tax bill. They can stage sales across years, harvest losses to offset gains, or place high-turnover strategies inside tax-deferred accounts.

Before you approve sweeping changes, ask, “What will this move cost me in taxes this year?” If the advisor cannot quote a rough dollar figure and outline a plan to cut it, the hidden fee is already on the way.

The investor’s quick-check playbook.

Now that you have unmasked the five biggest hidden fees, the next step is defense. A professional review should leave you richer in clarity, not poorer in net return. Use the playbook below whenever you engage an advisor or weigh a portfolio overhaul. Print it, tape it near your monitor, and refuse to skip a line.

- First, read every fee disclosure in daylight. Form ADV Part 2, custodian schedules, and fund prospectuses may not be light reading, but they list every dollar you owe if you know where to look.

- Second, translate percentages into cash. One percent of three-hundred-thousand dollars equals three-thousand dollars a year, not “only a point.” Saying the number aloud anchors the cost to reality.

- Third, insist on the “all-in” number. Advisory fee, fund expenses, platform charges, and projected taxes form one stack. Anything less invites surprises.

- Fourth, demand low-cost investment options. If a recommendation carries a higher expense ratio than a comparable index fund, ask why. Pay the upcharge only when the benefit is concrete and measurable.

- Fifth, verify fiduciary status and revenue sources. A true fiduciary earns only what you pay. Commissions, trails, or referral kickbacks signal a conflict you can avoid.

- Finally, monitor your statements. A quick quarterly scan can catch stray fees before they snowball. The habit takes minutes and often saves hundreds.

Turn fee fear into fee control.

Run this checklist and you turn fee fear into fee control. Every dollar you catch (a load, a trail, a platform surcharge, a tax you saw coming) stays invested and compounding instead of leaking out through a fee you never questioned.

That simple shift can preserve thousands of dollars over the life of your portfolio, returns no market forecast can promise. The advisor who welcomes these questions is worth keeping; the one who dodges them just told you everything you need to know.