The intersection of AI in banking and finance and lessons from logistics software may seem obscure at first glance. Yet, it holds a strategic key for financial institutions seeking to build AI-first systems that are resilient and operationally coherent. The logistics industry has long grappled with unifying fragmented data sources, orchestrating autonomous workflows, and managing real-time exceptions across complex networks, challenges that mirror those faced by banks today as they move beyond pilot projects toward enterprise-scale AI adoption. Specifically, modern logistics platforms are engineered to handle high-volume operations with extreme precision, anticipate disruption, and adapt in real time, offering a blueprint for banks to rethink how their own systems ingest, process, and act on intelligence at scale (and not just in isolated use cases). For engineers and architects, this is less about borrowing industry metaphors and more about understanding technical paradigms that have matured under heavy operational constraints.

Drawing on insights from the MIT Sloan Review on why banks should build cohesive AI strategies rather than scattershot deployments, a view backed by four pillars including data improvement and scaled infrastructure, we can extend those principles into actionable design patterns banks rarely consider For grounded guidance on real-world AI application in financial services, additional frameworks such as McKinsey’s AI-bank of the future offer complementary perspectives that align well with the logic of networked, autonomous systems.

The Hidden Parallels Between Banking Systems and Logistics Ecosystems

At their core, both modern banking and logistics systems manage complexity through interconnected workflows, continuous data flows, and operational decisions that should balance speed, accuracy, and risk. Logistics software was engineered from the outset to handle distributed assets and unpredictable conditions, which forced an architecture where data is fluid, orchestration layers are central, and exception pathways are first-class citizens. Banks, on the other hand, historically evolved from legacy ledgers and siloed systems, leading to pockets of intelligence that do not communicate effectively — a challenge highlighted by MIT Sloan as one of the main inhibitors to scalable AI adoption.

Logistics platforms maintain a real-time view of shipments, inventories, vehicles, and partners, continuously ingesting telemetry and external events (weather, delays, customs) so that decisions can be adaptive rather than reactive. In contrast, many banking environments still operate on batch cycles or asynchronous processes, which slow insight generation and inhibit high-speed decision-making models. Banks also struggle with disparate data domains (customer behavior, transaction streams, risk indicators), which makes unified model input pipelines difficult to establish, a core enabler of AI-first systems.

Both industries require precision: logistics should avoid misrouting goods that cost millions in delays, just as banks should avoid errors in risk scoring or compliance decisions that can erode trust and trigger regulatory penalties. Recognizing these parallels allows banking technologists to translate logistics patterns, such as unified data meshes and synchronous orchestration, into financial architectures that support real-time, continuous, and explainable AI behaviors rather than isolated experiments.

Lesson #1: Building a Unified Data Backbone Before Scaling AI

In logistics, a unified data backbone is not a luxury; it’s the foundation that allows autonomous systems to synchronize across thousands of nodes. Telemetry from vehicles, inventory levels, customer orders, and partner statuses all flow into centralized state stores that underpin optimization engines and predictive models. Without this backbone, logistics platforms would resort to brittle point-to-point integrations that fail in the real world. Banks, by contrast, often approach AI with fragmented data siloes based on product lines, channels, or departments, making it difficult to generate consistent, enterprise-wide insights.

A unified data layer for banking means consolidating transaction histories, customer profiles, risk metrics, and external data sources into a harmonized schema that preserves context. It is this contextual richness that turns raw information into intelligence, enabling models not merely to score but to reason across varied scenarios. When banks attempt to scale AI on top of fractured data assets, they inadvertently replicate the spaghetti-like integrations that have historically plagued core banking systems.

Consider how logistics systems use event streams and canonical models to track the state of goods and processes. Banks can apply the same technique by treating every financial event as a first-class entity in a real-time data mesh. This approach enhances situational awareness and enables models to operate against a single version of truth, improving both accuracy and trust. Industry resources, such as the Data Mesh paradigm, offer practical patterns for managing distributed data domains under a unified governance model.

Ultimately, a unified data backbone transforms banks from reporting entities into intelligent systems that can support continuous learning, real-time risk assessment, and pervasive orchestration across every workflow.

Lesson #2: Orchestrated Automation Beats Isolated AI Projects

A common anti-pattern in banking AI initiatives is deploying tactical models, a chatbot here, a scoring model there, without connecting them into an enterprise-wide workflow. This “AI à la carte” approach, cautioned against in the MIT Sloan piece, creates siloed pockets of intelligence that deliver incremental value but fail to shift the operational center of gravity. Logistics software, on the other hand, is inherently orchestrated: autonomous decision engines coordinate scheduling, routing, inventory movements, and exception handling in real time, reducing manual intervention and improving resilience.

Orchestration in an AI-first bank means establishing a control plane that sequences AI tasks, manages dependencies, and ensures consistency across multi-step business processes. For example, onboarding a new client involves identity verification, risk assessment, credit scoring, document ingestion, compliance checks, and portfolio assignment, a workflow that crosses multiple systems and decision points. Without an orchestration layer, banks simply bolt together these models with brittle integration logic that is hard to monitor, debug, or scale.

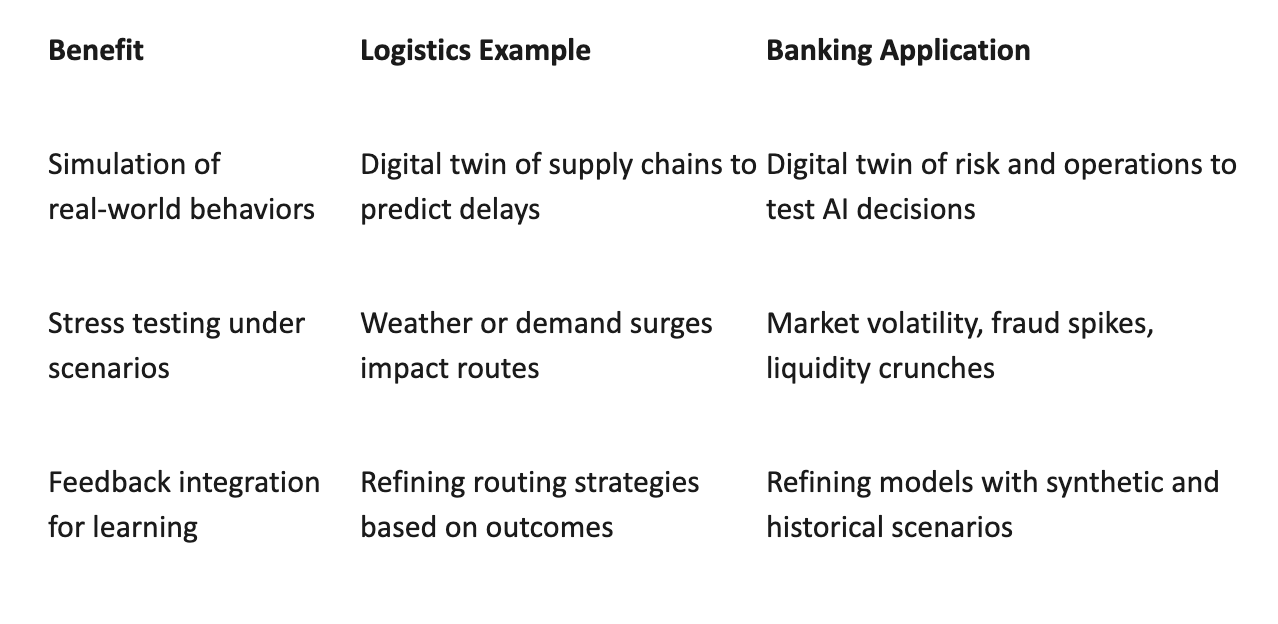

Lesson #3: Digital Twins Show Banks How to Pre-Test Complex AI Flows

Logistics organizations use digital twins, dynamic, high-fidelity simulations of physical assets and networks, to validate strategies before they touch real-world operations. In banking, digital twins are often used at a high level (e.g., economic models) but rarely as executable simulations of operational AI workflows. Adopting this pattern allows banks to test complex multi-agent systems involving risk, compliance, customer behaviour, and capital flows in a sandboxed environment. This reduces the risk of unintended consequences when models interact in unanticipated ways.

In logistics, digital twins ingest real-time and historical data to create a living simulation where AI agents optimize decisions. Banks can adapt these techniques to simulate scenarios such as liquidity stress, spike in fraud attempts, or regulatory demands in real time. By doing so, banks gain deeper insights into model behaviour, dependencies, and failure modes before exposing customers or regulators to potential risks.

Lesson #4: Logistics Software Treats Exceptions as Design Inputs, Banks Should Too

One of the key reasons logistics software is robust is that it assumes exceptions will happen and treats them as first-class design inputs. Route cancellations, carrier failures, and inventory shortages are built into orchestration logic so systems can adapt gracefully. In banking, suspicious transactions, compliance alerts, and liquidity anomalies are often handled as afterthoughts, bolted onto core processes with manual effort.

Designing for exceptions means building AI systems that don’t just detect anomalies, but adjust operational flows autonomously and transparently. This requires embedding exception patterns into orchestration logic and model-learning loops, so the system evolves in response to real-world conditions rather than reacting post-factum. Exception intelligence, where anomalies reshape future decision boundaries, enhances predictability, reliability, and governance.

Lesson #5: Real-Time Visibility Is the Cornerstone of Trustworthy AI

Real-time visibility is a hallmark of logistics dashboards that provide minute-by-minute updates across complex networks. Banks should achieve similar observability into AI decision flows to ensure trust, compliance, and performance management. Continuous visibility across models, data pipelines, and decisions empowers teams to detect drift, understand root causes, and enforce governance in line with regulatory expectations. Without real-time observability, banks are blind to emergent risks that can erode confidence and invite scrutiny.

Implementation Blueprint: How Banks Can Adopt Logistics-Style AI Maturity

To operationalize these lessons, banks can follow a phased blueprint:

Phase 1 — Unified Data Backbone:

Consolidate fragmented data into a real-time mesh with governance, lineage, and security controls.

Phase 2 — Orchestration Layer:

Build a centralized engine that sequences decision workflows, manages dependencies, and handles outcomes.

Phase 3 — Digital Twin Sandboxes:

Develop simulated environments to test multi-agent AI workflows against real-world scenarios.

Phase 4 — Exception Intelligence:

Implement feedback loops that adapt models and workflows when exceptions occur, rather than triggering manual follow-ups.

The Strategic Payoff: AI-First Banking Built on Logistics Principles

By learning from logistics software, banks can transition from isolated AI pilots to resilient, integrated, and continuously adaptive AI-first systems. This shift unlocks operational coherence, real-time responsiveness, and a competitive edge in an era where leaders are rapidly pulling away from the pack.

Disclaimer: The information provided in this article is for general informational purposes only. It is not intended as legal, financial, or professional advice. All views expressed are those of the author and do not necessarily reflect the official stance of any organizations or companies mentioned. Readers are encouraged to seek advice from qualified professionals for specific concerns.